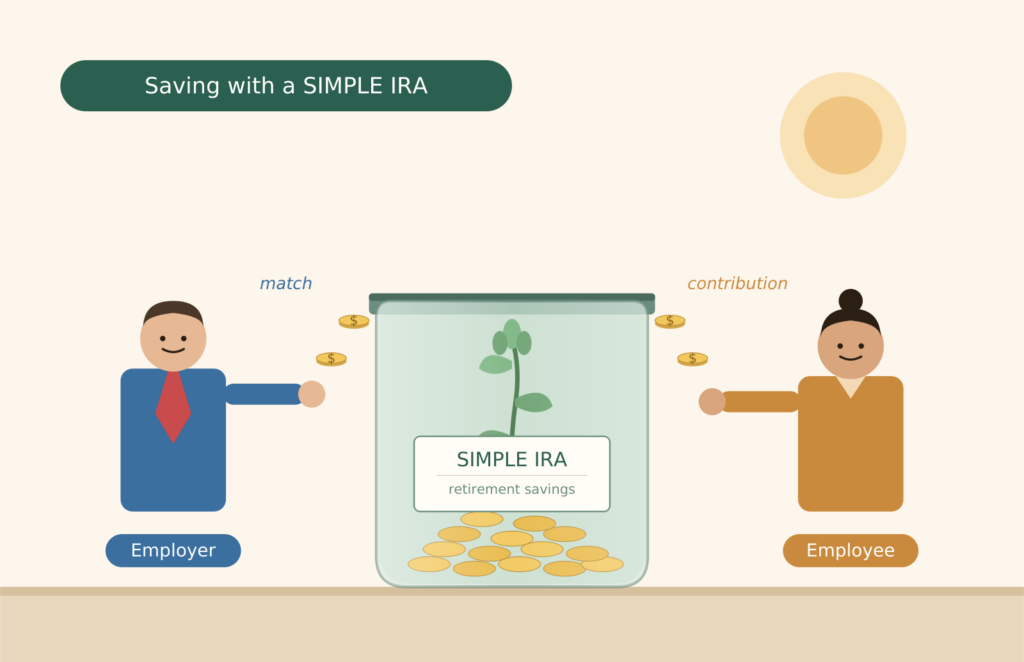

The SIMPLE IRA is the Savings Incentive Match Plan for Employees. The SIMPLE allows for both employer contributions and employee deferrals. The plan is ideal for employers who want to contribute something — but not a lot — to employee retirement accounts.

This is the second in a two-part series about retirement plans for the small business. The first was about the SEP IRA.

Who Is Covered Under the SIMPLE?

The SIMPLE is for an employer with fewer than 100 employees who earned less than $5,000 in the previous year. The employer cannot have any other retirement plan — only the SIMPLE. Any employee who earned $5,000 in any of the previous two years and expects to do so in the current year is eligible to participate. The plan must be established before October 1st for the current year. After October 1st it will become effective for the following year.

Employer Contributions

A big part of retirement plan design has to do with discrimination. The IRS wants to be sure that the plan does not discriminate — meaning that the plan’s benefits are available across the board to all employees, both management and rank-and-file. Two safe harbors exist for the employer to make non-discriminatory contributions: the 2% rule and the 3% rule. An employer can choose which to use.

The 2% Rule

The employer contributes 2% of payroll to all eligible employees. This is subject to a $350,000 salary cap (2026), so the maximum 2% employer contribution will be $7,000.

The 3% Rule

The employer makes a 3% of payroll matching contribution only to those who choose to defer into the plan, up to the $350,000 (2026) salary cap. If Employee A deferred 3% of his earnings, the employer would match with an equal amount, capped at $10,500.

Employee Deferrals

The maximum employee deferral allowed is $17,000 (2026). Those over age 50 can defer an additional $4,000, for a total of $21,000. Under SECURE 2.0, employees aged 60–63 may make an enhanced catch-up contribution of $5,250 instead of $4,000, for a total of $22,250.

All contributions vest immediately. There is one unique feature to the SIMPLE, though: any transfers, distributions, or rollovers made during the first two years incur a 25% tax penalty — not the usual 10% penalty before age 59½. The clock starts running when the first deposit hits the account.

If you participate in a SIMPLE IRA, you may still be eligible to make your own Traditional or Roth IRA contribution. Deductibility of the Traditional IRA depends upon income limits and coverage under other qualified plans. Roth participation depends upon income limits.

A Good Place to Begin

The SIMPLE, then, as I see it, is a good way for an employer to give something to his employees, and to give them an opportunity to defer. From the employee’s point of view this is “free” money — a benefit that the employer chooses to give over and above salary. Each participant has his or her own IRA and makes his or her own investment choices. Upon separation from service the SIMPLE balance — after two years — can be rolled into a personal IRA or a qualified plan with a new employer.

Other related blog posts you may find interesting are: Did You Start a Business and the SEP IRA for Self-Employed.