With this blog post I’m beginning a two-part series about retirement savings plans available to the small business owner. In this piece I’m going to explain the Simplified Employee Pension, or SEP IRA. It is best used in a small shop, with few (or no) employees. It can be established by an individual proprietor filing a Schedule C, or by a corporation, LLC, or partnership. In this piece I’m going over the rules for a SEP established by a corporation, where everyone — including the owner — is a corporate employee.

There are different rules for the self-employed, who file a Schedule C. Please see our companion piece, SEP IRA for the Self-Employed.

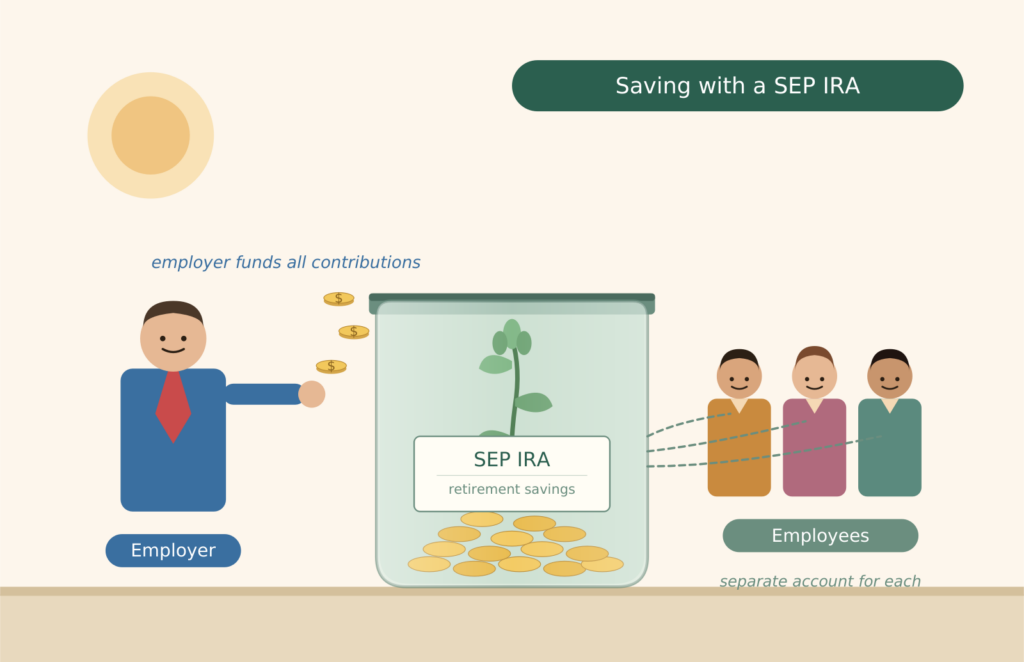

The SEP — Simplified Employee Pension

The SEP is designed for the business owner with few employees. Money goes into the SEP from employer contributions only — there is no opportunity for employee deferrals. All contributions are tax-deductible to the employer. A SEP IRA account is opened for each participant, and all funds contributed are immediately vested. (There is an older version, called a SARSEP, or salary reduction SEP. Although many are still out there, they cannot be opened after 1996.)

The employer must cover those employees who are age 21, have worked for the employer for any three out of the five preceding years, and work more than 600 hours per year. Quick math: 600 hours at 40 hours per week is 15 weeks.

Figuring Contributions

The contribution is as much as 25% of each person’s payroll, up to the maximum contribution allowed by the IRS — $70,000 in 2026. Whatever percentage of payroll the employer contributes to his own account must also be contributed to the employees’ accounts. Say the owner has W-2 income from his own corporation of $100,000, and he pays two part-timers who each earn $20,000. The employer may contribute $25,000 to his SEP account, and then must contribute $5,000 to each employee account.

Can you see how the SEP is best for very small businesses? As a rule, the small employer is going to want to limit benefits paid to employees to the minimum needed to attract qualified employees. On the other hand, if all the employees are family members, contributing the same percentage across the board may be perfectly acceptable, if not desirable.

There is flexibility in contributions year-to-year. An employer may contribute the maximum one year, or even nothing at all another year. The key point is that the contribution percentage of earnings must be consistent across all covered employees in a given year.

Let’s Look at the Taxes

First Scenario — No Contribution

Assume no SEP contribution, and W-2 income of $100,000. The taxpayer is married filing jointly, so the standard deduction is $32,200 (2026). Taxable income is $67,800, and the federal tax due is approximately $7,659.

Second Scenario — Maximum Contribution

What if that business owner instead made a maximum SEP contribution of $25,000? Now his Adjusted Gross Income is $75,000. After the $32,200 standard deduction, taxable income is $42,800. The federal tax liability is now approximately $4,659. This is a tax reduction of $3,000! Another way to look at it: it only costs $22,000 to make a $25,000 SEP contribution — an immediate return of roughly 13%.

For the Sole Proprietor

The contribution rules are a little different for the proprietor, who has no separate business entity — the owner whose taxpayer ID and Social Security number are one and the same. In this case the maximum contribution works out to be about 18.59% rather than 25%. This has to do with the fact that the SEP contribution is subtracted from the business gross income to arrive at net income. Please see our companion piece, SEP IRA for the Self-Employed, to see how this works.

Other Considerations

An employer may very well be able to contribute the maximum to his SEP, and also contribute to a Traditional IRA or Roth IRA — the limits are separate, though the Traditional IRA may or may not be tax-deductible depending on income.

Often business owners split their income between W-2 and dividend distributions in order to save on self-employment taxes. In the above examples, the corporate business owner may want to pay himself $50,000 in W-2 income and take the other $50,000 as a dividend distribution. There are several pros and cons here:

- Qualified dividends are taxed at capital gains rates — 0%, 15%, or 20% depending on taxable income. For 2026, the 15% rate applies to most middle-income married taxpayers.

- Self-employment tax isn’t paid on dividend distributions, reducing immediate tax burden — but this can also reduce Social Security benefits in later years.

- A lower W-2 income means a lower potential SEP contribution, since the contribution is based on a maximum 25% of payroll, not dividend distributions.

- A lower W-2 income means a lower Social Security payment in retirement. Are you kneecapping your ultimate Social Security benefit to save a few dollars today?

Other related posts you may find useful: