We usually understand the time value of money in two contexts: the growth rate of an investment, and the inflation rate. Nonetheless, the TVM is a topic that should be understood by everyone serious about financial planning.

Sketch Out a Timeline

To conceptualize this, sketch out a timeline of your life. At the leftmost point is your date of birth. The rightmost point is your date of death. In between, mark your retirement date, and today’s date. If you are not yet retired, then the time value of an investment pertains to you in particular.

TVM: Investment Growth Rates

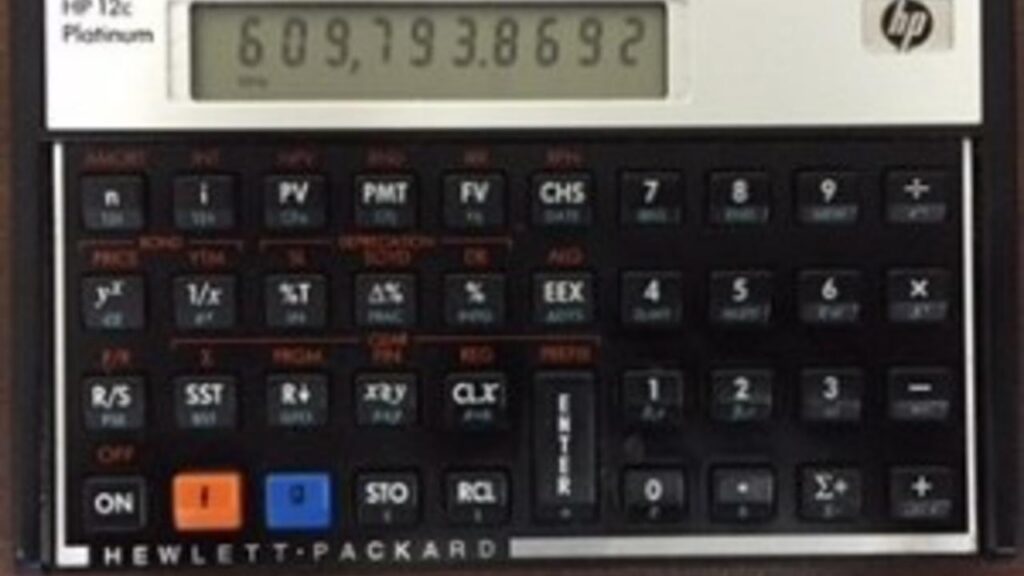

Let’s look at investment growth rates. On your timeline you have 10 years before your retirement. You’re interested in projecting out your IRA balance over these 10 years, assuming an 8% annual rate of return, compounded monthly. Your current balance is $250,000, and you are depositing $300 per month — less than what is permissible by law. I make the following entries on my HP 12-C calculator:

- Present value: −$250,000

- Payment: −$300

- Interest: 8% ÷ 12

- Time (number of compounding periods): 120 (10 years × 12 months/year)

The result: $609,793.87

The future value of that investment, then, is nearly $610,000. The calculation is linear — it assumes that each dividend and dollar of interest received is reinvested at 8%, and that underlying securities prices increase by 8% evenly each year. Is this a useful calculation? Yes, by all means — it is a place to start. Knowing that market returns are never a straight line but rather a jagged one, perhaps over time an 8% average is a fairly useful projection number. Indeed, over the 25 years ending in 2020, the S&P 500 (a portfolio of 100% stocks) averaged close to 10% annually.

TVM: Inflation Rates

Back to the timeline you conceptualized above. What is important if you’re to the right of your retirement date? You want to pay attention to both investment growth and inflation.

The retiree’s biggest risk is, of course, running out of money. That unhappy circumstance would have to do with various factors: rates of return on investment, inflation rate, rates of spending, and so on.

What retirement costs will inflate? Gasoline, groceries, health insurance premiums, prescription costs — in short, many things. If you go into retirement with a mortgage, that monthly payment won’t change, unless you have a variable rate mortgage. Here’s a personal example: when I was in college, I purchased gas for $0.259/gallon. On a morning in early 2020, gas was $2.159/gallon — a 5.6% average annual increase over approximately 42 years. Pretty stiff. Did you ever imagine paying nearly $5 for a loaf of bread?

Inflation Is One of Your Greatest Financial Risks

The clear implication for the retiree is this: Will your income keep up with inflating prices on the things and services you need to purchase over the next 30 years? Anyone retiring today at age 65 could easily have a 30-year retirement ahead, if not longer. That is a long time for investments to work.

This is where financial planning is key. Once you retire, your investments are both earning and being depleted at the same time, as you draw down the balance for living expenses. The word to the wise: factor in an appropriate inflation rate, and be very careful and intentional with one’s planning.

For information on working with CameronDowning, please see our Investments Frequently Asked Questions.