How to Qualify for a Mortgage

Time to buy a home? Congratulations! Qualifying for a mortgage depends upon many factors: qualification ratios, credit scores, credit history, the property being purchased, etc. In this article I’m focusing on the qualification ratios.

Two Qualifying Ratios

There are two that lenders use: the front-end ratio, usually 28%, and the back-end ratio, usually 36%. The front-end ratio means that no more than 28% of your gross income – gross, not take-home – should cover your mortgage payment, property taxes, insurance, and any association monthly fee. The back-end ratio, often 36%, should cover all that plus any recurring debt payments, such as a car payment, student loan payments, or credit card payments. In the case of credit cards, the lender factors in the required minimum payment, and not the higher amount you may be accustomed to sending in.

Is there any leeway with the ratios? Often yes, for those with strong credit scores, and particularly with the back-end ratio. We’ve heard of these at 50%, which in our opinion would be insane – you’d be living to support your house payments. You’d be working for your house, in other words, rather than your house supporting you.

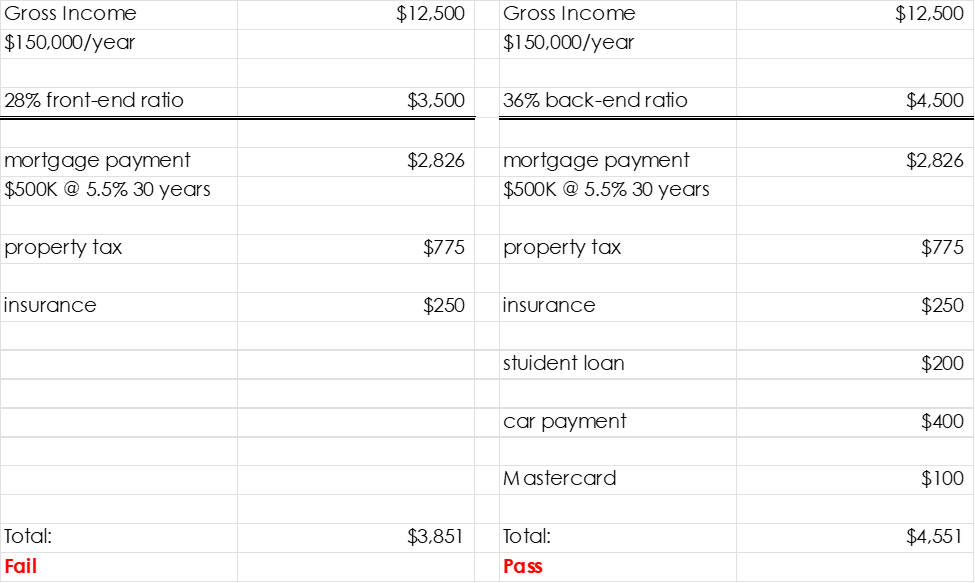

Failing One Ratio but Passing the Other

This buyer is looking to purchase a home that is not in a neighborhood association for $625,000. He is bringing $125k cash to the closing table, which is a 20% down payment. No mortgage insurance involved here.

This is an example of how the applicant can fail one mortgage ratio but pass the other. The annual income is $150,000, which is $12,500 on a monthly basis. At 28%, the total housing costs should not exceed $3500/month. At 36%, total housing costs plus debt payment should not exceed $4500/month.

Please see the chart above. The applicant fails the first test – the 28% allows only $3500 for total housing costs, and we’ve estimated $3851. A little arithmetic tells me that this applicant would need a gross income of $165,043 to make this work.

The second test is off by only $51, so I’ll call that a pass. This is the ratio that is the most flexible. In fact, with good credit scores we’ve heard of lenders going up to 50% on this ratio. Of course, you’d be house poor – you’d be working to support your house, rather than the other way around, but if you don’t mind eating hot dogs every night maybe things would work out okay. We’d never actually recommend a client use 50% for this ratio – 38% to 40% tops.

You can get a good idea from this illustration how to prepare yourself for a mortgage application. Are your ratios within range? If not, you could work to pay off a car note, or student loan. Once you’ve got your mortgage and closed on your home purchase, no one will ever follow up with you, meaning you’re free to finance a new car or run up new debt.

Interested in learning more? I’ve written several pieces about real estate purchases: