by Glenn J. Downing, MBA, CFP®

Q: I have a lot of high interest credit card debt. Should I take out a 401k loan?

This is a question we come across not uncommonly. There is a lot to like about doing this, but a big potential tax trap as well. I want to distinguish clearly between 401K loans and 401K withdrawals. In this piece I’m discussing the loans. In Part II I’ll go over the withdrawal option.

What are the Rules?

First of all, your 401k plan has to have loan provisions in place. No loan provisions, no loan. An employer can always go to his third-party administrator to have the plan documents amended if he would like to make loans available to the employees. The loaned amount can be 50% of the vested account balance up to $50,000. A special rule allows participants with smaller balances to borrow up to $10,000 without the percentage restriction.

How Do I Obtain the Loan?

From what we’ve seen, plan participants simply log on to their retirement accounts, and there is a tab there to initiate a loan and input banking information. The loan has to be approved by a committee, and within a few days the funds show up in your bank account.

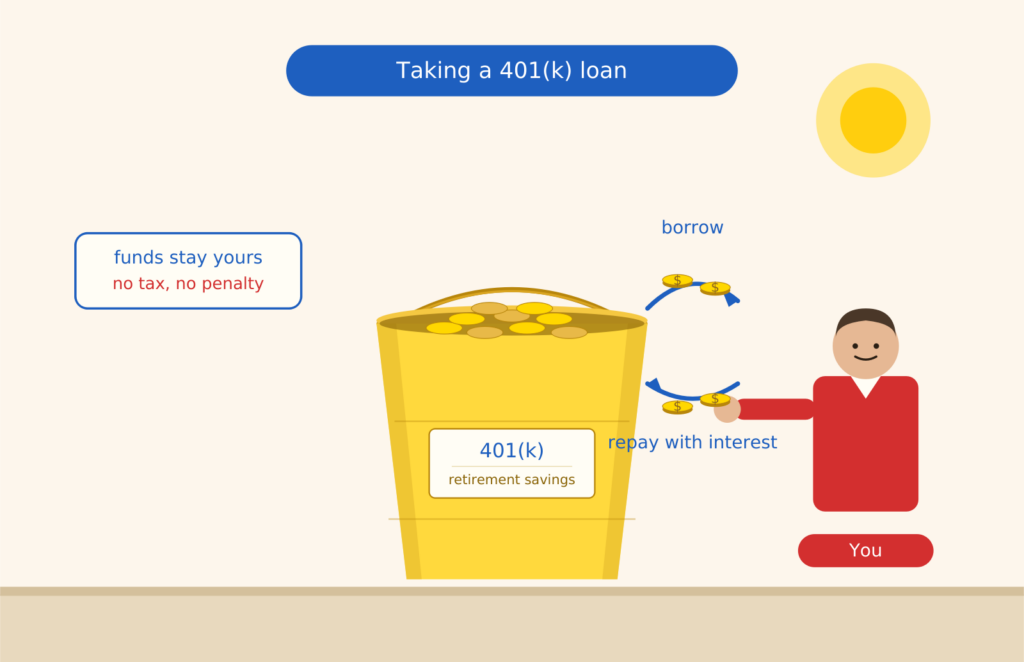

You’re Paying Yourself Interest

Any 401K loan has interest attached. Typically there’s a variable formula, as in LIBOR plus a couple of points – currently we are seeing 11% as common. Certainly less than your credit cards. So yes – using a 401K loan to pay off high interest credit cards makes great sense on the face of it.

There is an opportunity cost here. Say you’re invested in a S&P 500 Index fund which returns 12%. Your loaned money will only return the 11% interest that you are paying. By virtue of having taken out the loan, then, you’ve forfeited 1% return on the funds loaned out. There is also a strategy here: as you allocate your portfolio among the conservative, moderate, and aggressive choices, consider the loaned amount to be your conservative allocation. That means you perhaps can go more aggressive on the remaining funds.

How Do I Pay It Back?

Through payroll withdrawals. When you apply for the loan you’ll apply for a repayment period, typically 24, 36 or up to 60 months. You’ll see how much will be withheld from each paycheck. If you are using the funds to swap out high interest debt, then you can adjust your budget to reflect the lower income amount offset by the payoff of the credit card(s).

What are the Risks?

First, that you’ll run the credit card balance back up. This is a behavioral issue. Many people who use a HELOC (home equity line of credit) to consolidate debt then feel like they are out of debt – and then the old behavior returns. This is a significant risk.

Second, that you lose your job and the loan becomes due. This is the potential tax trap. Any amount not repaid becomes a taxable event. Say you lose your job and default on your payments. You have a $5,000 outstanding balance. You won’t have to repay the loan, but now the 401K plan reports this $5,000 balance to the IRS as a distribution. That means the $5,000 is fully taxable to you, along with a 10% early withdrawal penalty if you’re under 59½. Let’s use an example: The $5,000 isn’t repaid, and you are age 45 and in a 22% tax bracket. You’ll owe ($5,000 × .22) and ($5,000 × .10) or an additional $1,600 in taxes that year. Not the end of the world, but you wouldn’t choose it.

If you change employment you can roll your current 401(K) balance to your new employer’s plan. Then you have until October of the following year (tax filing date plus extension) to replace the loaned funds in your new 401(K).